“No asset wins forever: What a decade of market data teaches us about building resilient portfolios”

Cdr S Thankappan (Retd), CFP®

Over the past decade, investors in India have witnessed multiple market cycles: liquidity booms, economic slowdowns, global crises, rate shocks, and sharp recoveries. Yet despite living through these events, many portfolios remain poorly diversified, overly dependent on one asset class, and vulnerable to predictable mistakes.

Recently, I analysed the market data available for the period commencing 2015 to date and constructed a multi-asset performance roulette, complemented by an asset leadership matrix and an asset risk matrix. The studied data covered Indian equities (large, mid, small), Gold, Real Estate (REITs), and Cash. The goal was not to predict the next winner, but to understand a far more important question: What does history teach us about building resilient portfolios?

The insights were striking, and in some cases, deeply counterintuitive.

Data Source

The available data in case of “Equities” (large-cap, mid-cap and small-cap) and “Gold” for the period were downloaded in csv format from NSE/yahoo finance portal. Data in respect of “Cash” was obtained from the return chart of ETF ‘LiquidBeeS’ and requisite yield was derived using the indicated python file. “Real Estate” data was appropriated from the performance return of REITs introduced in India in 2019. Hence the absence of Real Estate as an asset class till 2019 in the performance roulette.

The python file used for generation of the insights is Performance Roulette by Asset Class.ipynb - Colab

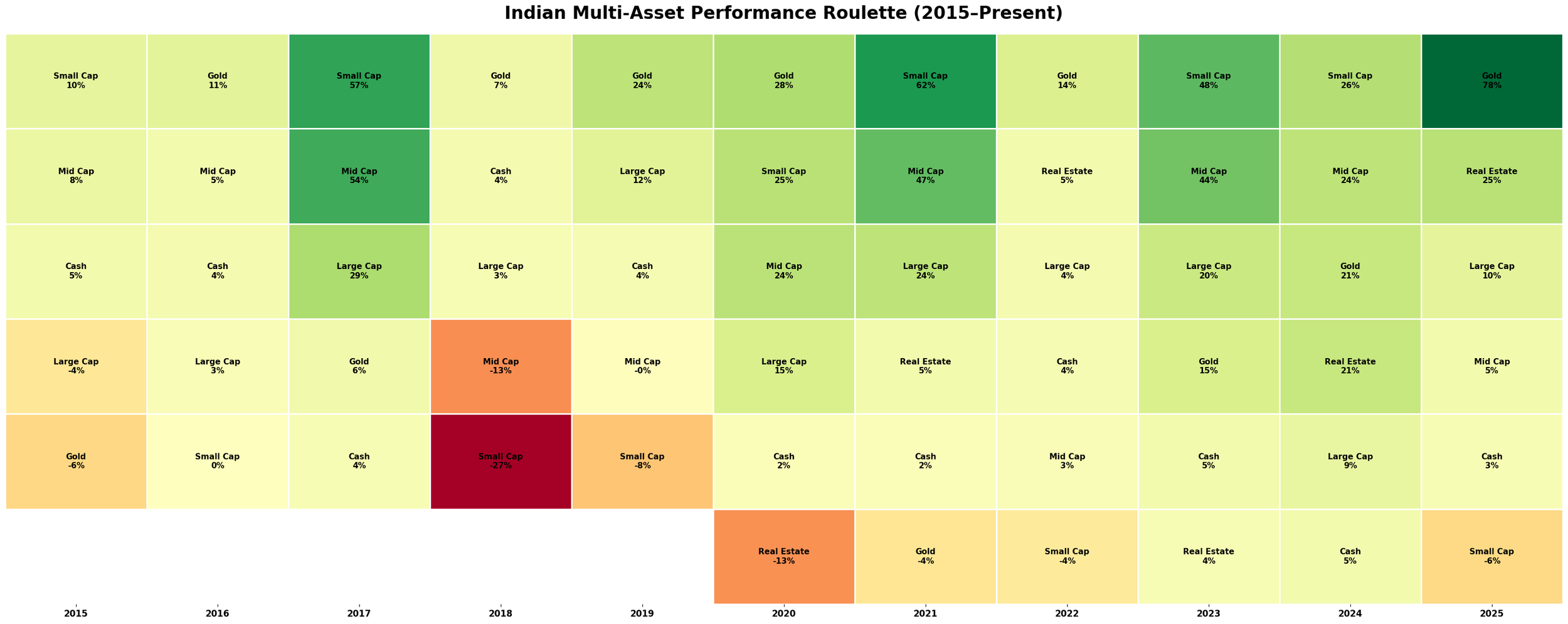

Performance Roulette

Best Performers by Year

2015 - Small Cap 2016 - Gold 2017 - Small Cap 2018 - Gold 2019 - Gold 2020 - Gold

2021 - Small Cap 2022 - Gold 2023 - Small Cap 2024 - Small Cap 2025 - Gold

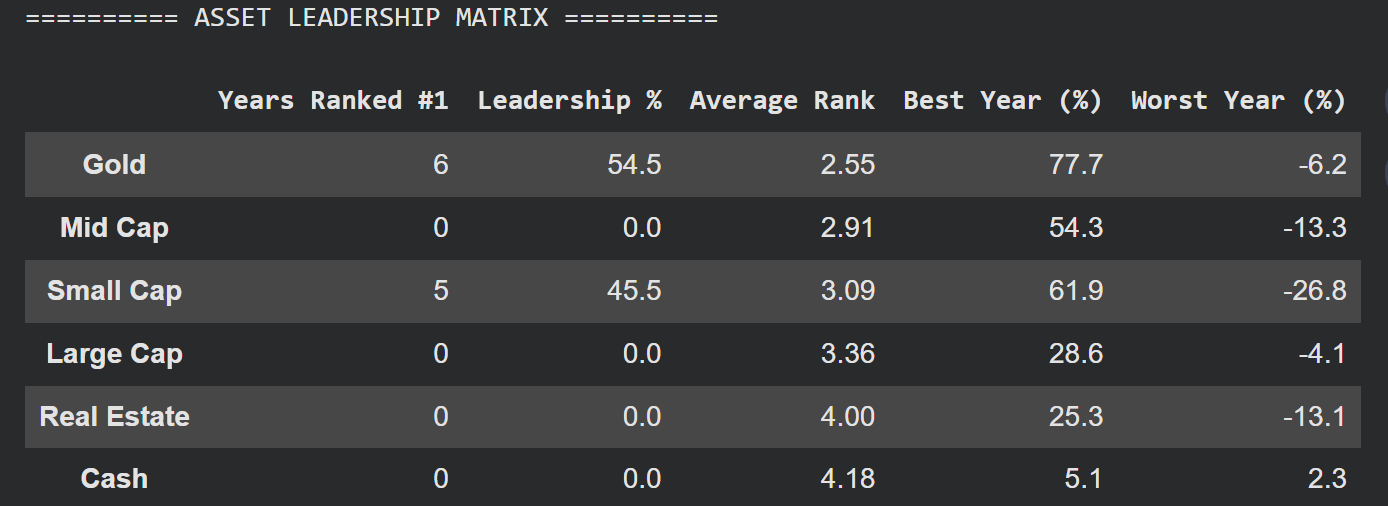

Asset Leadership Matrix

Key Insights

Gold top-performer for 6 years

Small Cap top-performer for 5 years

Highest return ever in a year - Gold

Largest draw-down in a year - Small Cap

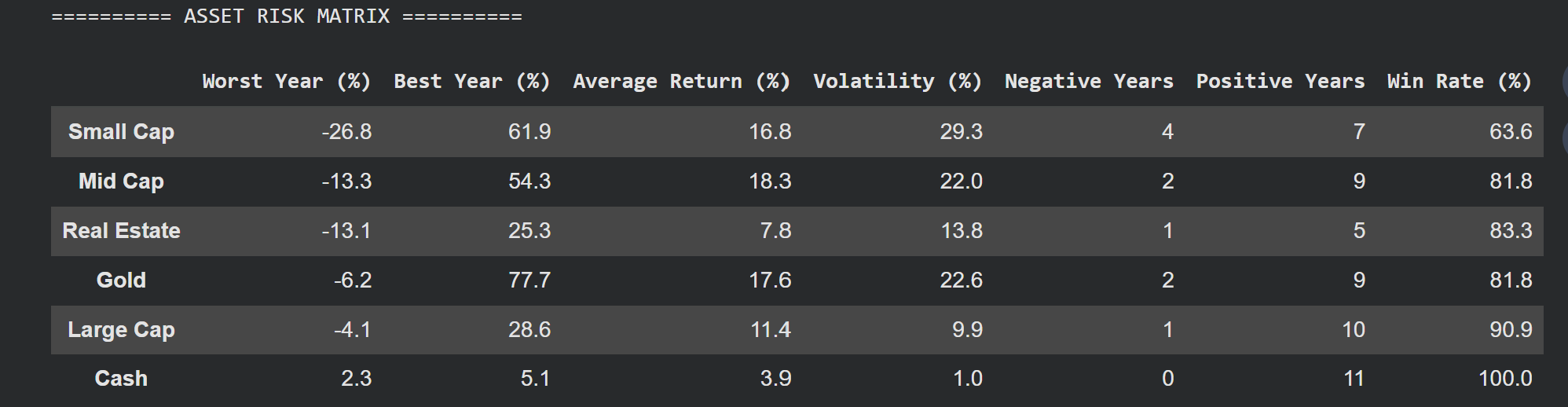

Asset Risk Matrix

Key Insights

Highest Volatility - Small Cap

Max Negative Years - Small Cap

Max Positive Years - Large Cap

Lesson 1: Leadership always rotates

Perhaps the most powerful visual from the performance roulette is the constant rotation in asset leadership. No single asset class dominates across years. Small caps may lead dramatically during liquidity-driven expansions. Gold often surges when uncertainty rises. Large caps tend to stabilize portfolios during stress. Cash quietly preserves optionality when risk assets stumble. This pattern is not random but structural. Economic growth, inflation, interest rates, global capital flows, and investor sentiment move in cycles. Assets respond differently to each phase. Expecting one asset class to outperform indefinitely is less an investment thesis and more an act of optimism. Yet investor behaviour repeatedly ignores this reality. After a few years of strong performance, capital floods into the recent winner. Portfolios become concentrated. Expectations extrapolate recent returns into the future. Then the cycle turns.

The roulette reminds us of a simple but uncomfortable truth: Outperformance is temporary. Diversification is permanent.

Lesson 2: The best asset is rarely the most comfortable

The asset leadership matrix revealed another critical insight: the assets that create the most wealth are often the hardest to own. Small caps frequently rank at the top. But they also appear near the bottom during difficult years. Their journey is volatile, emotionally taxing, and requires patience.

Large caps, on the other hand, rarely dominate the leaderboard. Yet they consistently avoid catastrophic outcomes. Over time, this stability becomes incredibly valuable. Gold tells a different story. It may spend years appearing irrelevant, until crisis strikes. Then it does exactly what it is supposed to do: protect purchasing power and provide psychological comfort when other assets falter. Cash almost never leads. But leadership is not its job. Cash provides liquidity, optionality, and the ability to rebalance when opportunity emerges. In volatile markets, that flexibility can be priceless.

This leads to a deeper realization: Portfolio construction is not about picking the most exciting asset. It is about combining assets you can actually hold through a full cycle.

Lesson 3: Average rank matters more than occasional victory

Many investors obsess over which asset finishes first each year. But institutional allocators focus on something far more meaningful: consistency. An asset that occasionally delivers spectacular returns but frequently collapses can destroy investor behaviour. Panic selling during drawdowns permanently impairs wealth. Conversely, an asset that rarely finishes last contributes enormously to long-term compounding by reducing behavioural mistakes.

In other words: The goal is not to own the annual winner. The goal is to avoid owning the perennial loser.

Lesson 4: Drawdowns shape investor outcomes more than returns

If the performance roulette shows opportunity, the asset risk matrix shows reality. Every asset class carries a “personality”: a characteristic pattern of decline during adverse periods. Some assets fall fast and deep. Others decline modestly. A few may even rise when panic spreads. Here is the crucial point: Investors do not abandon portfolios because of low average returns. They abandon them because of sharp losses. Drawdowns are not merely statistical events. They are emotional events. When portfolios fall significantly, rational plans collide with human psychology. Fear replaces discipline. Long-term strategies dissolve into short-term reactions. This is why professional allocators ask a different question than most investors: Not “What will I earn?” But “What is the worst that can happen?”

The answer determines whether a portfolio is survivable.

Lesson 5: High returns mean nothing without survivability

One of the most dangerous misconceptions in investing is equating higher returns with superior portfolios. Consider two hypothetical assets:

· Asset A delivers higher long-term returns but suffers deep periodic crashes.

· Asset B generates slightly lower returns but with far smaller drawdowns.

Mathematically, Asset A may appear superior. Behaviourally, many investors will fail to hold it. And an asset you cannot hold is an asset you cannot benefit from. This is why risk-adjusted thinking separates professional investors from speculators. The objective is not maximizing theoretical return.

The objective is maximizing realized return: the return investors actually capture by staying invested.

Lesson 6: Cash is not a drag - It is strategic flexibility

In bull markets, cash is often mocked. It appears unproductive while equities surge. But the matrices reveal a more nuanced role. Cash is not designed to compete with risk assets. It is designed to create optionality. When markets fall, cash becomes dry powder. It allows investors to rebalance into cheaper assets without selling into weakness. In institutional portfolios, cash is rarely viewed as idle. It is viewed as strategic flexibility.

And flexibility is a form of risk management.

Lesson 7: Gold’s value lies in crisis, not popularity

Gold’s role becomes obvious only when it is needed: which is precisely why many investors under-allocate to it. During stable growth periods, gold may lag equities. Questions arise about its relevance. But when uncertainty spikes during periods of inflation fears, currency volatility or geopolitical stress, gold often behaves differently from financial assets. (Like present times)

That difference is diversification. Diversification does not mean owning many assets that move together. It means owning assets that respond differently to stress. Gold earns its place not by winning every year, but by protecting portfolios when confidence erodes. Insurance always feels unnecessary, until it becomes indispensable.

Lesson 8: Real Estate adds a distinct dimension

REITs introduce an interesting hybrid characteristic: part growth, part income, part rate-sensitive. They remind us that diversification is not just about adding more equities under different labels. Assets influenced by varied forces create resilience. A portfolio heavily concentrated in a single economic outcome is fragile, regardless of past returns.

Lesson 9: Cycles are inevitable - Forecasting them is not

Many investors believe success comes from predicting which asset will lead next. History suggests otherwise. Cycles are certain. Timing them is not. Rather than attempting precise forecasts, professional portfolios prepare for multiple outcomes simultaneously. They accept uncertainty instead of trying to eliminate it. Diversification is not a concession to ignorance. It is a recognition of reality.

Lesson 10: Asset allocation drives outcomes more than security selection

Study after study has shown that long-term portfolio behaviour is dominated by asset allocation rather than individual security choices. The matrices reinforce this principle. Owning the right mix of growth, defensive, and hybrid assets matters far more than finding the next multi-bagger. Security selection may add incremental alpha, but asset allocation determines whether the portfolio survives long enough to compound.

Lesson 11: Simplicity often outperforms complexity

An interesting takeaway from multi-asset analysis is that robust portfolios do not require excessive complexity. A thoughtful blend of equities, gold, real estate, and cash already introduces meaningful diversification. What matters is not the number of holdings, but the diversity of economic exposures. Over-engineering of portfolios can create the illusion of sophistication while adding little resilience.

Clarity beats complexity.

Lesson 12: Behaviour is the ultimate risk factor

Markets fluctuate. That is their nature. But the greatest threat to long-term wealth is rarely the market itself. It is investor behaviour. Chasing recent winners. Selling during declines. Abandoning strategy mid-cycle. A well-diversified portfolio is not merely a mathematical construct - it is a behavioural tool. By smoothing the investment journey, it increases the probability that investors stay the course. And staying invested is the single most powerful driver of compounding.

The Final Lesson: Diversification is not about maximizing returns - It is about minimizing regret

When viewed together, the performance roulette, leadership matrix, and risk matrix converge toward one overarching insight: No asset is reliable enough to deserve your full conviction. But a thoughtfully diversified portfolio does not require certainty. It requires balance. There will always be an asset you wish you owned more of in hindsight. That is unavoidable. Diversification ensures that regret is manageable rather than catastrophic. And investing, at its core, is often the art of managing regret.

Closing Thought

Investors frequently search for the “best” asset class - the one that will outperform next. History suggests that this pursuit is misguided. The real objective is not identifying a perpetual winner. It is constructing a portfolio capable of navigating multiple futures. Because the future will not resemble the recent past. It never does. In the end, successful investing is less about brilliance and more about discipline - the discipline to diversify, to respect risk, and to remain invested across cycles. The matrices do not tell us what will happen next.

But they do teach us something far more valuable: Resilient portfolios are built not on prediction, but on preparation.

Disclaimer

The data used in this study has been sourced from publicly available databases, index providers, and market-linked instruments believed to be reliable. Certain asset classes are represented using indices or market proxies (such as ETFs/REITs) where long-term investable benchmarks are unavailable. These proxies are intended to approximate asset class behavior and may not perfectly reflect actual investor returns.

The analysis relies on calendar-year returns and does not incorporate taxes, fees, slippage, inflation, or portfolio rebalancing costs, all of which can materially impact realised outcomes. Additionally, changes in index composition, regulatory frameworks, market structure, and economic conditions over time may affect comparability across periods.

This study is retrospective in nature and is designed to illustrate broad market patterns rather than provide precise performance measurement.

This article is intended solely for educational and informational purposes and should not be construed as investment advice, a recommendation, or an offer to buy or sell any securities or financial instruments. The analysis is based on historical data, and past performance is not indicative of future results.